Market Correction of 2016

You may have noticed that the stock market has had a rough few weeks to start the new year. Including yesterday’s (Jan 20, 2016) selloff, the S&P 500 Index is down 9% for the year and 11.9% from a recent high made in November. To use some technical jargon, this means that we have reached a “correction” (a decline of 10% or more) but not yet a “bear market” (decline of 20% or more).

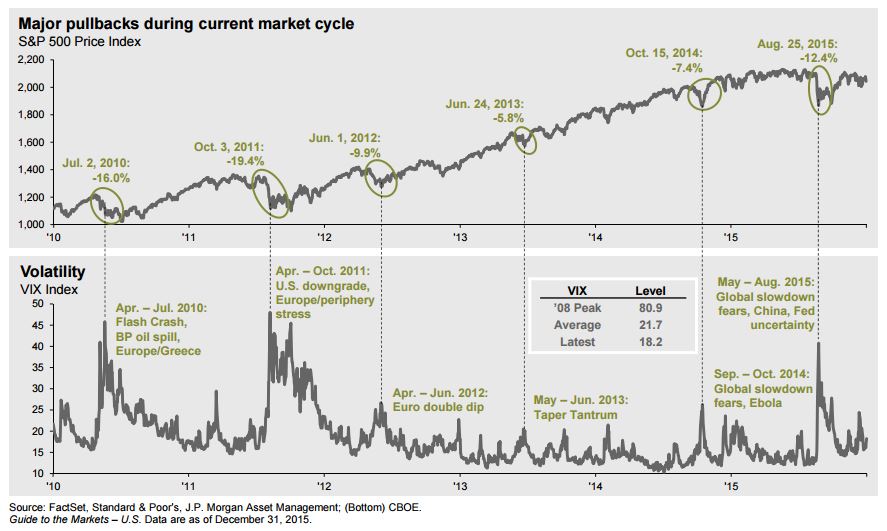

Although market corrections and bear markets are not pleasant experiences, they are a normal part of investing. In the last 36 calendar years, there have been 20 years with a 10% stock market decline. Even during the very robust stock market growth since the 2008-2009 decline, there have been five corrections while the S&P 500 has more than doubled in value. You may recall some of these corrections. Some had to do with the BP oil spill, the flash crash, the downgrade of U.S. Treasury debt rating, and man-made crises involving shutting down the government and raising the debt ceiling. If you only have a slight memory of these other corrections, there’s a chance that this too will be another “calamity of the day” that we will soon forget.

However, there’s always the chance that this will develop into a bear market. There have been 8 bear markets since World War II. Many of these bear markets have occurred during some combination of: recessions, commodity spikes, aggressive Federal Reserve actions, and extreme valuations (bubbles) in stocks or real estate. We certainly don’t see a commodity spike today. The Fed recently raised interest rates from 0% by a quarter of a percent for the first time in 9 years, hardly aggressive by any definition. Although stocks have had a nice run over the past 7 years, their prices as they relate to earnings have been near the long-term average. A recession could be in our future, but the 7 year recovery has been very stable thus far with slower than expected growth for a recovery, but quite consistent.

The question we often hear during tumultuous times like these is “shouldn’t we be doing something about this?” The answer is both yes and no. Yes, because we should plan for market volatility by not investing all of our nest eggs in stocks. Some allocation should be made to bonds to minimize the volatility and give us a safer place to take income from while stocks are down. We should also regularly rebalance the accounts by selling the investments that have performed well recently and use the proceeds to buy the investments that are lower and thus more likely to outperform in the future. This means selling stocks after the good times, harvesting gains and putting them away in stocks. It also means selling some of our bonds in times like these to take advantage of low stock prices.

The answer is also no, we shouldn’t do anything about this as long as we have already done the advanced planning. Nothing has happened that we believe will permanently change most investors' ability to reach their retirement goals. The one thing, above all else, that would change your retirement would be to pull out of the market (locking in these temporary declines) and then try to figure out how and when to get back in.

Sometimes people wonder why we're perpetually optimistic about the future of their investments. One key reason is because history is on our side! Even with the huge ups and downs that we've experienced in investment markets over the years, the trend has always continued upward. Anyone who thinks otherwise is making that forecast based on speculation. It is possible that the future won't be like the past, but I would much rather base my outlook on historical trends than by guessing.